Dynawatt: 12 GW Exits the CAISO Queue

July 5, 2026 · Twenty-four projects, mostly gas, dropped out of California's interconnection queue this week. The rest of the digest is nuclear licensing paperwork and loan announcements. Very little

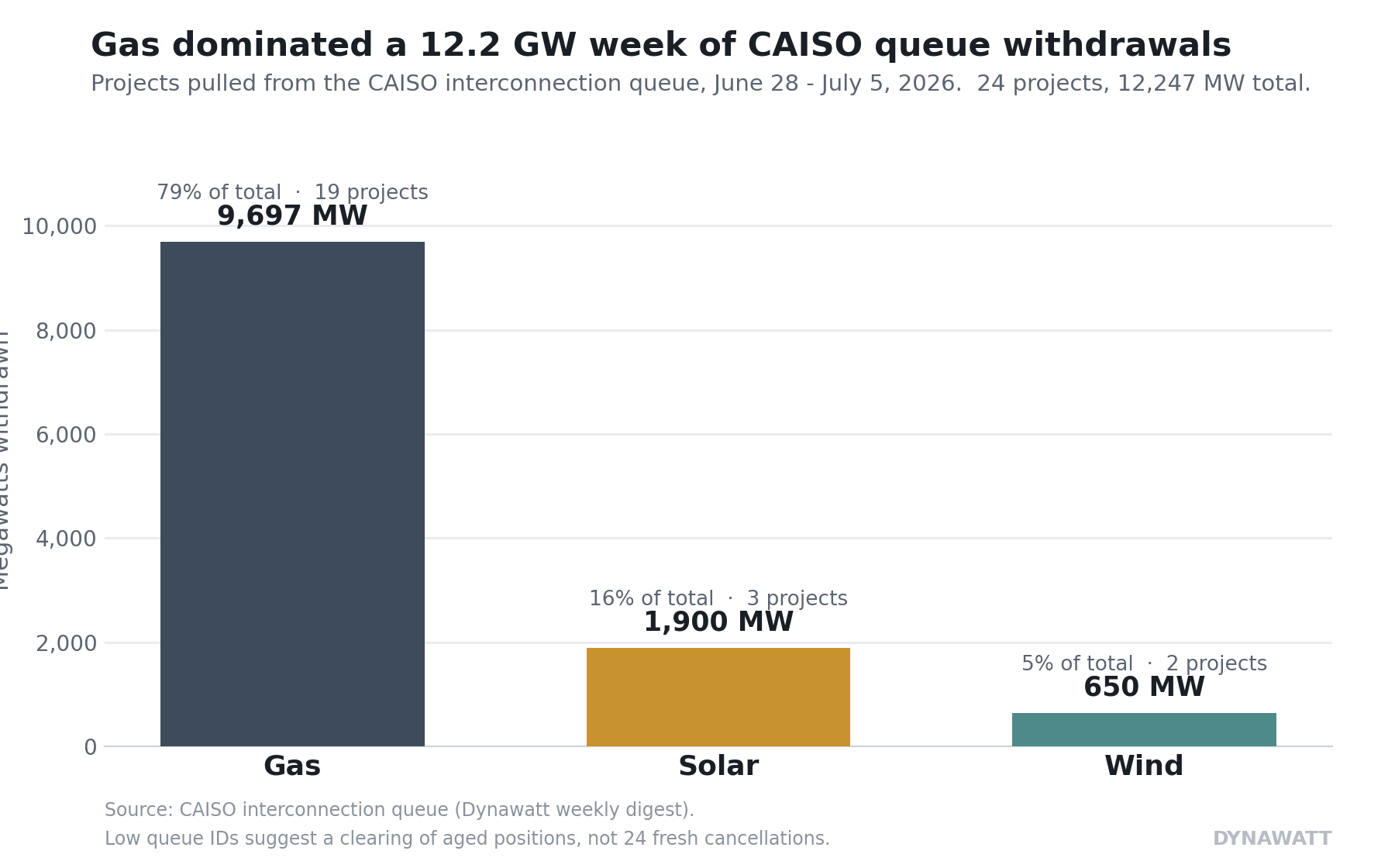

Ninety-six items this week, and almost all of it sits on the supply side. The one clean dataset is a wave of withdrawals from the CAISO interconnection queue: 24 projects, 12,247 MW, and 79% of that capacity is gas. Everything else is process. Dozens of NRC licensing filings, most of them routine, and a batch of DOE loan announcements, several of which look recycled. If you came looking for megawatts headed toward the large loads we track, there aren't many here.

The one hard number: 12.2 GW out of CAISO

The withdrawals break down as 9,697 MW of gas across 19 projects, 1,900 MW of solar across three, and 650 MW of wind across two. All but one sit in California. The outlier is a 634 MW gas plant in Clark County, Nevada.

Before reading this as 12 GW of live projects collapsing in a week, look at the queue IDs. They run low, from the 250s into the 450s, and several of the names belong to plants that are already operating or were shelved years ago: Marsh Landing, La Paloma, Antioch, Oakley. This reads as CAISO clearing aged, stale positions, not two dozen developers pulling the plug on the same Tuesday. Treat it as housekeeping until the queue-reform status confirms otherwise.

Housekeeping or not, the composition says something. What washed out was overwhelmingly gas, in the ISO where gas has had the hardest time advancing in the first place. California’s queue is where thermal proposals sit and then vanish. This week a batch of them vanished at once.

Nuclear: motion, not megawatts

By item count, most of the digest is NRC activity. Topical reports, withholding determinations, decommissioning filings, security rulemakings, SMR pre-licensing. The pipeline flagged nearly all of it as routine, and that’s the right call. It’s licensing throat-clearing, years away from any electron.

A few items carry more weight. Constellation filed a subsequent license renewal for R.E. Ginna in upstate New York, which is about keeping existing baseload alive rather than adding to it. The NRC opened environmental scoping for two SMR units at Palisades in Michigan, a real if early step. And the single item that touches our beat directly is buried in the stack: the comment period for Constellation’s license amendment at the Crane Clean Energy Center, docket 05000289, with comments due July 8. Crane is the former Three Mile Island Unit 1, the 835 MW restart tied to Microsoft’s data-center power deal, targeted for 2027. The digest doesn’t flag that connection, but it’s the one operating-nuclear-meets-data-center story on the board, and this week it surfaced as a routine comment window. Motion, not megawatts.

DOE reopens the loan window

DOE’s Loan Programs Office is active again. The digest reports its first clean-energy loan guarantee in nearly a decade, a first conditional commitment for advanced fossil energy, a $2B tribal energy solicitation, and a grid-reliability loan closing. Read this cluster with caution. Some items carry stale framing (one still references the “Biden-Harris Administration,” another is the 2024 Ultium battery guarantee), so at least part of the batch looks recycled rather than fresh. The signal that survives: federal financing for firm and grid capacity is flowing again. That’s money, and money sits a long way upstream of a built megawatt.

Reading the signal

One theme runs through the week. It’s all supply side, and it splits cleanly into subtraction and paper. Gas left the CAISO queue in bulk. Nuclear advanced on paper. DOE reopened the checkbook. None of it puts firm capacity on the system in the near term.

Note what’s absent. The large-load demand side, the ERCOT Large Load Working Group we treat as the primary read on data-center demand, surfaced nothing this week, so there’s no fresh demand print to set this supply activity against. What’s left is lopsided: the queue is shedding thermal capacity, the firm-power hope is migrating to SMRs that are years of licensing away, and the one restart tied to a real data-center offtake showed up as a comment deadline. The gap between the load-growth story and deliverable firm megawatts did not close this week.

The one to watch: whether the CAISO withdrawals are a queue-reform purge. If CAISO confirms a batch cleanup of aged positions, the 12 GW is administrative and the real story is how much dead gas was still nominally in the queue. If any of these are genuine live-project cancellations, that’s a harder read on building thermal capacity in California, and worth pulling the individual queue records.

Dynawatt is an independent brief compiled from public sources (ISO/RTO interconnection queues, FERC notices, ERCOT Large Load Working Group, PJM stakeholder committees, NRC ADAMS, and DOE Loan Programs Office announcements). It is informational, non-advocacy, and not investment advice.