Dynawatt — California Is Building Storage and Solar, Not Firm Power

May 31–Jun 21, 2026 · Developers filed 34.6 GW of interconnection requests in three weeks. Firm, around-the-clock power is 3.6% of it.

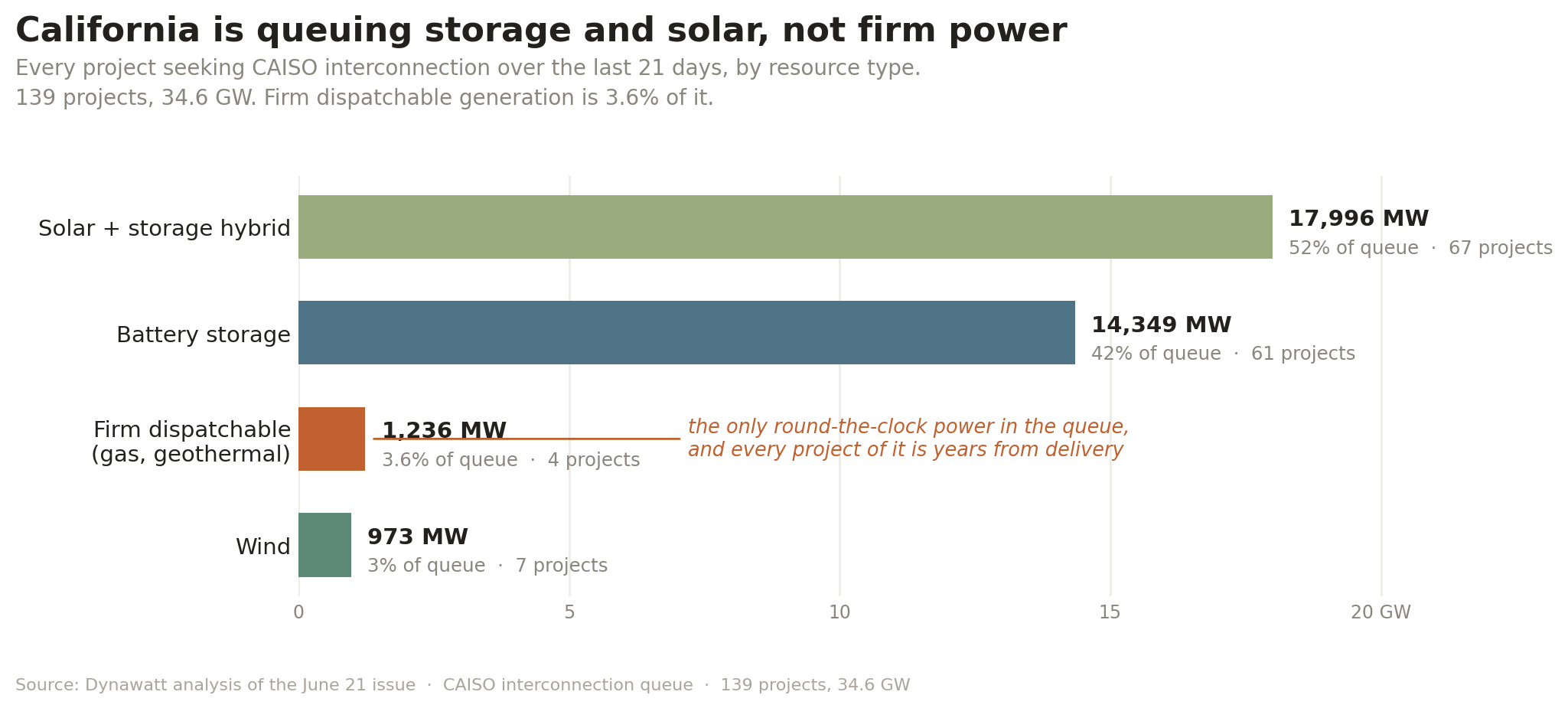

Over the last 21 days, developers filed 139 new interconnection requests with CAISO, totaling 34.6 GW. That is an enormous amount of capacity to queue in three weeks. Almost none of it can run around the clock, and that gap is the story for anyone tracking where AI load is going to get its power.

The queue in one breakdown

The composition is lopsided in a way that matters. Solar-plus-storage hybrids account for 17,996 MW, 52% of the queue across 67 projects. Standalone batteries add another 14,349 MW, 42% across 61 projects. Put those together and storage paired with solar is 94% of every megawatt seeking grid access in California right now. Firm dispatchable generation, the kind that produces power at 3am regardless of sun or wind, comes to 1,236 MW, just 3.6%, across four projects: three gas plants, the largest a 590 MW combined-cycle unit, and a single 53 MW geothermal facility. Wind is the remainder, under 3%.

Reading the signal

Most of this queue is not capacity. It is timing. A battery generates nothing. It moves existing power from one hour to another. The 18 GW of solar-plus-storage and 14 GW of standalone batteries piling into this queue are built for a single job: smoothing California’s midday solar glut into the evening ramp. They firm a renewable grid, and they do it well. They add close to nothing that a flat, constant load can draw on after dark.

The firm power that exists is tiny, and all of it sits years away. Filter the queue to its most material projects and the firm names do rise into view: a 715 MW gas combined-cycle plant, a 501 MW combustion turbine, a 500 MW steam-and-storage hybrid. But every one of them is at queue entry, the very start of a CAISO interconnection process that routinely runs several years. The projects actually crossing into operation this cycle are batteries and solar. So the supply reaching the grid now is intermittent, and the firm supply is still a filing.

For a data-center load, that is the wrong build on the wrong clock. AI demand is flat and round-the-clock, the opposite of the duck-curve problem storage solves, and it is landing in the next 18 to 24 months, faster than a gas plant clears interconnection. California is pouring 34.6 GW into its queue, and the sliver that actually matches the shape of the incoming demand is the part furthest from delivering a watt. The queue is not failing to grow. It is growing in the wrong direction for this particular load.

What’s not in the data

A limit worth stating outright, because the framing depends on it. All 139 of these projects are CAISO. There is no ERCOT here, no PJM, and not one large-load interconnection filing, which means the demand half of the story still is not in the numbers. The closest thing is a single line in one gas-plant summary guessing the unit “may support data-center demand,” and that is speculation, not a disclosed contract. So read this as what California’s supply queue reveals, not as the national load picture. The national picture needs the ERCOT and PJM feeds, and those are not landing in these pages yet.

What to watch

Two markers. Whether any of the firm thermal advances out of queue entry, because that is the first real sign California is treating 24/7 load as a generation problem rather than a storage one. And whether ERCOT’s large-load filings finally surface here, because that is the demand all of this supply is implicitly racing. Until both appear in the same issue, you are reading one side of the market and inferring the other.

Sources

CAISO Public Queue Report, the full queue these 139 projects are drawn from: https://www.caiso.com/library/public-queue-report

Browsable, daily-updated view of the same data:

https://www.interconnection.fyi/?market=CAISO

Queue data ingested via gridstatus.io. Individual projects are listed by queue position in the CAISO report.

Dynawatt is an independent brief compiled from public sources (ERCOT Large Load Working Group, ISO/RTO interconnection queues, FERC & Federal Register filings). It is informational, non-advocacy, and not investment advice.